The pandemic has led to a striking deterioration of finances, both for corporations and households alike. And if you need to contact debtors who fail to repay in time, you can use artificial intelligence and machine learning to support the process.

In this post, we talk about how AI can improve debt collection, discussing the benefits of using it in your business.

How to use AI in debt collection

Some 191 million Americans now have credit cards, with total consumer credit exceeding $14.9 trillion. If lenders are to stay afloat, they need effective ways to collect the debt.

Here are five ways you can use AI in debt collection.

1. To improve communication

Debt collection is a sensitive subject. And it’s not always easy to reach borrowers. But AI-powered tools, like chatbots, don’t just help lenders make contact. They actually improve the quality of communication.

Chatbots and virtual assistants work across platforms (including email, text messages, Facebook Messenger, WhatsApp, Telegram, and other apps). Meaning that, by investing in AI, you can scale your outreach without losing the human touch, all while keeping a cap on your overheads.

Better still, you can tailor each message to the individual. Say, by sending reminders when you know a debtor is online or tweaking the tone of the message depending on the recipient’s age. The best AI tools can even mimic the user’s style based on their chat history.

Moreover, some people prefer to talk on the phone — while others favor messages over phone calls.

That said, if you have the right data, you can pinpoint each customers’ preference, then tailor your strategy to boost both response and collection rates.

2. To streamline processes

Unwieldy business processes are one of the most significant barriers to excellent customer service. And banks are no exception.

But you have the power to make debt collection quick and easy by shifting the process online instead of making customers come to the bank. You could even automatically email invoices straight to the borrower.

By implementing artificial intelligence, you align your processes with customer expectations. And this not only includes sending messages at the most appropriate times. It covers choosing what message to send.

AI can factor in whether it’s the first reminder or not, then choose a text message template based on the context.

3. To better understand customers

The average American household has $8,701 of credit card debt. At the same time, most people have at least two credit cards, alongside student loans and mortgages.

If you want to fully understand your customers’ borrowing profiles, you need a single overview of their debt history across different banks and services. And that’s almost impossible to achieve manually.

But if you use AI, you can analyze data from various sources, uncovering crucial insights about your customers’ credit history.

4. To optimize your debt collection strategy

AI-powered tools can also improve human decision-making in debt collection. The software works with historical data about solvent and insolvent borrowers, making it easier to spot at-risk accounts.

You’ll start seeing patterns that flag potential late or non-payers, enabling you to implement a proactive, not reactive, strategy.

5. To modernize analytics

Artificial intelligence aggregates data from diverse sources. Meaning companies can significantly improve the quality of their business intelligence by integrating AI and ML solutions into their debt collection process.

Algorithms process datasets in ways that humans cannot. In some cases, the algorithms extract concrete patterns from the data. In others, the data is a black box that an algorithm can ‘open’ via various model explainability techniques.

An experienced data science team can analyze the models’ output, drawing your attention to bottlenecks, even using ML to find optimal strategies based on the type of debt you collect or your organization’s financial goals.

Either way, by using AI in finance, you can adapt to the digitization of banking. With over one billion online credit card transactions happening every day, you need cutting-edge tools and techniques to help you keep pace in a digital world.

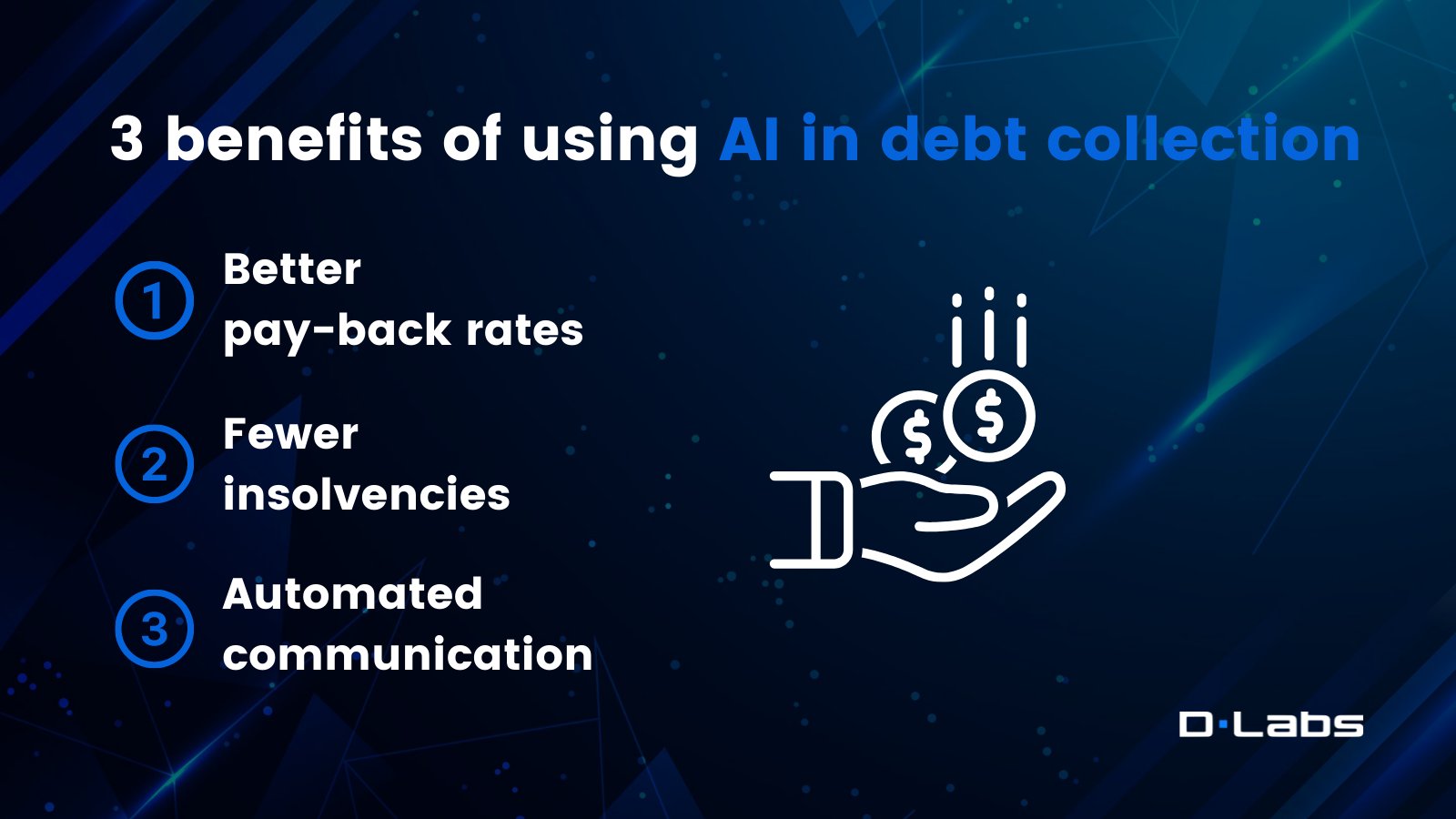

3 benefits of using AI in debt collection

Artificial intelligence makes processes like debt collection more efficient, which leads to several benefits. Here are the three most common improvements:

1. Better pay-back rates

Every year, banks suffer huge losses from credit defaults. Loans go unpaid, and financial institutions find themselves in difficulty. But if you use AI for predictive analytics, risk assessment, and fraud prevention, you can reverse your fortunes, even boosting profits up to 38%.

AI can help you understand your customers and develop better outreach strategies, ultimately translating to better pay-back rates.

2. Fewer insolvencies

Traditionally, banks implement measures to motivate borrowers to repay loans after a missed payment. A more effective approach could be to deploy a system that spots at-risk profiles before the delay ever happens.

Such systems can even let you assess whether an individual should get a loan in the first place, helping you avoid lending to risky clients instead of negotiating repayment schedules later on.

3. Automated communication

Thanks to AI, you can now find the best channel to reach customers on, then automate the outreach. Imagine using a chatbot to ping clients on social media when you know they’re online.

That’s the most effective way to ensure they get the message.

In short, using AI in debt collection helps banks avoid major credit risks. And while it will always be impossible to predict all possible outcomes, you can certainly reduce losses and improve the customer experience with the right tools.

Use Cases: AI in debt collection

Now we’ve covered how you can use AI in debt collection, let’s look at some case studies that demonstrate using it in practice.

Automated phone calls for alimony collection

RadiCall is a Polish start-up that helps parents to collect alimony from their ex-partners. There are more than 300,000 alimony non-payers in Poland, which means that roughly a million children don’t get the financial support they deserve.

DLabs.AI worked with the company to develop a minimum viable product, carrying out closed testing before the product was made public.

We developed an AI-enabled web app to automate alimony collection, using the available contact information to make regular calls on a predefined frequency as soon as there’s a missed payment.

The client can customize the message they want to send, and the app takes care of the rest. Users have praised the app’s effectiveness, saying it’s helped them collect more money from their co-parents.

Chatbot for debt collection

Bank of America uses a chatbot called Erika to streamline customer service without compromising on quality. Clients activate the service from within the bank’s app using text or voice.

One service that Erika provides is debt collection, helping customers make down payments or consequential payments. In the background, the chatbot constantly checks for offers, sending personalized messages if there’s the chance to reduce debt or save money.

Erika adds to the friendly, customer-centric strategy of the bank. Michelle Moore, Bank of America’s head of digital banking, even said Erika is helping consumers establish a better relationship with money.

Financial scoring for decision-making

GiniMachine is an automated AI decision-making platform that helps banks boost their expertise, while you can also use the tool to update outdated business processes.

The platform lets you score clients’ debt-paying ability, building effective predictive AI models in the process. That means you can now decide whether to approve or reject a credit application in seconds based on credit history and other data.

You can even deploy new collection strategies like calls, texts, or messages on social media, whatever works best for you.

Time to put your knowledge to work

Artificial intelligence is a powerful debt collection tool.

Whether you use it to increase customer engagement, improve communication, or update outdated processes, there are many ways it can help you turn your debt resolution process into a user-friendly experience.

Better still, by implementing AI, you’ll open a path to better business intelligence and borrower analytics, ultimately giving you more detailed profiles of the people you’re lending to.

Add this to a predictive analytics toolset, and you’ll be primed to spot risks and recover more debt, setting your business up for success.

If you’re considering using AI for debt collection, we bet you’d like an idea of what that may cost. That’s why we’ve prepared a short guide to give an outline estimate.

See the potential time and cost of your AI project by clicking this link.